Climate Change Reporting: Bank Impacts

Aakash Pansari, Senior Product Manager, Climate Change, Oracle Financial Services | May 22, 2023

Climate change is one of the most significant societal shifts of our time. And there has been a commensurate increase in awareness and recognition of the impacts posed by the anticipated changes. Based on the 2015 Paris Agreement and a 2018 report issued by the Intergovernmental Panel on Climate Change (IPCC), it is imperative to limit the increase in global temperature to 1.5°C.

Financial services are emphasizing the importance of capturing and distributing reliable, comparable, and transparent climate change data through improved reporting. Beyond that, the industry is faced with making significant changes. Nowhere is this more acute than in how banks will redefine “sustainable growth” in a future likely marked by the constriction of capital flows to the highest polluting sectors.

The change is already underway—as part of the Net-Zero Banking Alliance (NZBA). Over 129 banks, representing 41% of global banking assets ($74 trillion USD), have committed to financing and achieving a net-zero transition.

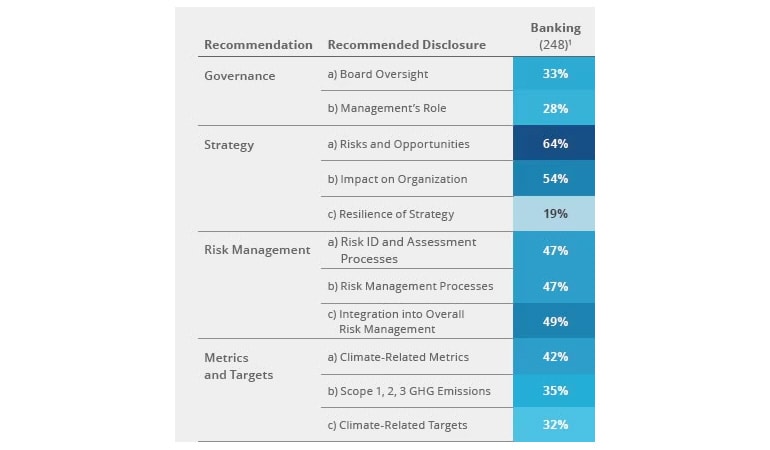

Increased spotlight on banks

Banks are increasingly coming under the lens of regulators and government agencies for their role in funding climate change via their investments, popularly referred to as financed emissions. Banks finance the global economy and may fund projects and activities that release harmful Greenhouse Gas (GHG) emissions, ultimately leading to climate change.

raditionally, banks have focused on managing risks like credit, liquidity, reputation, regulatory, etc. However, climate-related risks still need adequate consideration by banks. According to a study by Carbon Disclosure Project (CDP), financial institutions are underestimating the cost for the most significant climate change-related risks, a potential financial impact of over $1trillion USD.

As per GHG Protocol Corporate Standard, climate change reporting mainly focuses on greenhouse gas (GHG) emissions disclosures classified into three categories: Scope 1, Scope 2, and Scope 3. Scope 1 and 2 emissions result from an entity’s captive and purchased energy sources. Meanwhile, Scope 3 emissions are all other indirect emissions that occur in the value chain of reporting entity. Owing to the very nature of their business, banks would naturally not have significant Scope 1 and 2 emissions to disclose. For banks, the devil lies in Scope 3 emissions. Per CDP’s estimate, banks’ financed emissions amount to over 700 times their direct emissions (Scope 1 & 2).

Urgency to standardize climate change reporting requirements

The global investor community is increasingly curious for information on climate change-related risks and opportunities from stocks, bonds, and other securities. Over the years, the landscape of climate change reporting has seen a plethora of various frameworks and standards, including the Task Force on Climate-related Financial Disclosures (TCFD), Global Reporting Initiative (GRI), Principles for Responsible Investment (PRI), Sustainable Development Goals (SDGs), and Integrated Reporting Framework (IR).

These climate-change reporting frameworks are mostly voluntary in nature and often suffer from a critical shortcoming of comparability. For investors who have worldwide exposure, their need for reliable, comparable, and transparent climate change reporting is missing.

Emergence of the big three—ISSB, ESRS, and U.S. SEC rules

To streamline the climate change and sustainability reporting landscape, 2022 proved to be a landmark year with the introduction of the Big Three regulatory guidelines:

- U.S. Securities and Exchange Commission (SEC): Draft rules were released in March 2022, with a focus on climate change

- International Sustainability Standards Board (ISSB): Two proposed standards were released in March 2022, with a focus on climate change

- European Sustainability Reporting Standards (ESRS): Twelve draft standards were released in April 2022, with a focus on sustainability, including climate change

These climate change disclosure reporting frameworks are built on four core principles that aim to provide users with (1) vital information related to a firm’s governance and risk management policies, (2) quantitative metrics on GHG emissions, (3) climate targets, and (4) forward-looking scenario and resiliency analysis. Currently, companies publish ESG or climate disclosures on their own timelines, which can be six, nine, or 12 months after year-end reporting. A major change proposed in the climate change reporting standards is to disclose information within an entity’s annual reports to ensure a common timeline, enhance credibility, and address timeliness concerns.

Here is a subset of the climate change reporting requirements focused on the quantitative nature of the standards:

- GHG emissions across Scope 1, 2, and 3 categories

- Emission reduction targets

- Financial effects from material physical and transition risks, and opportunities

- Climate-related scenario analysis

- GHG emissions intensity

- Internal carbon price

- Carbon credits/offsets

- Sustainable finance targets

- Industry-specific disclosures for banks

Impacted companies and expected timelines

Acknowledging the implementation challenges for climate change reporting, each standard has a phased timeline for adoption. For example, U.S. SEC rules have a phased approach until fiscal year 2026, while ESRS is set for 2028.

These standards are applicable based on each entity’s metrics, such as asset size, revenue, or number of employees.

- U.S. SEC is applicable for all SEC registrants, including foreign private players

- ESRS covers most of the larger European Union (EU) companies and non-EU companies or groups with significant operations in the EU

- ISSB is likely to be used by the rest of the world based on adoption by individual jurisdictions and/or regional versions of the base standard, like the acceptance of IFRS accounting standards

How Oracle can help you with climate change reporting requirements

Oracle Financial Services offers a cloud-native, SaaS climate change analytics solution to help meet requirements for internal, statutory, and management climate change reporting. Its solution covers cross-jurisdictional requirements for ISSB, ESRS, U.S. SEC, and TCFD, embedding climate change risk into the overall risk management framework and supporting future investment and business decision-making based on climate change targets. With Oracle, customers gain access to 100+ out-of-the-box climate change reports, can easily perform ad-hoc analysis, and drill down to the most granular level of data.

Interested in exploring Oracle Financial Services Climate Change Analytics solution